The British Columbia Provincial Sales Tax (PST) is a retail sales tax. It is charged on most goods and services that are acquired, purchased or brought into the province of British Columbia.

Formerly called the Social Services Tax (SST), it applies to the purchase of both old and new products or services in BC. If a resident of BC buys or leases taxable goods from outside BC, the PST gets applied (and payable) when it is brought into BC.

In this blog post, we will be explaining how the PST applies to real property contractor within the construction industry in BC. If you are a contractor or subcontractor in the construction industry in BC, this is for you.

When done reading this blog article, you will be well informed on what the PST is all about, how it is applied, and how to go about it.

Before we take a deep dive into the meat and potatoes of this article, let us first define some key terms that relate to the BC PST.

What is Real property?

Real property is a piece of land or anything that is affixed to land, such that it becomes an integral part of that land (real property) afterwards. Typically, this includes structures, buildings and items such as equipment and machinery that are attached to structures and buildings via a means other than their weight.

Who is a Contractor?

According to the BC bulletin for real property contractors, anyone who engages in the supply, fixing or installation of goods that becomes a part of a real property is seen as a contractor.

This definition applies to all subcontractors and contractors alike within the construction industry. The rule of thumb to follow in determining if you are deemed a contractor (that’s duty-bound to pay PST) is a simple one.

If you check any of the boxes below, then you are a contractor:

Supply goods and render installation services on said goods, such that they become part of real property, and…

Supply goods in the line of providing you services to a client, such that it becomes a part of real property. Examples are electricians, plumbers, carpenters, fence builders, roofers, window installers, painters, etc.

Some other examples of contractors who are duty-bound to pay PST in BC are:

Excavators

Foundation contractors

Kitchen installers

Heating system installers

Sheet metal contractors

Siding contractors

Sundeck builders

And much more…

How Does PST Apply To Contractors?

As a contractor or subcontractor, in the course of rendering your services to clients, you are viewed as the end user of the materials being used to fulfil the contract. As a result of this, you are to pay the PST on such taxable goods - and NOT charge your client PST.

You are also mandated to pay PST on taxable goods acquired and used for fulfilling contracts on real properties that are outside of BC.

When Do you Collect PST?

There are specific scenarios where you are not the end user and must collect PST on taxable goods. Listed below are some of those scenarios:

If you install goods that do not become an integral part of real property. An example of this is supplying and installing a potted plant for a client in his building or structure.

If you are a contractor, who sells goods without installation services, that is, you run a retail or wholesale facility that solely focuses on the resale of concerned goods.

How to Pay PST

You can remit the PST you owe, as well as those charged to clients, to the government through either of the following means:

You can use any of the channels listed above to remit your PST to the government if your business has $1.5 million or less in total Canadian lease and sales volume for the year in view.

For sales volume above that, the payment must be made electronically.

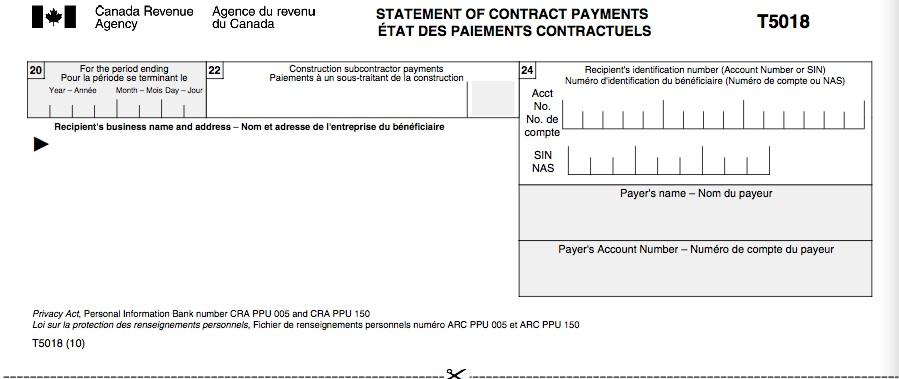

The T5018 is an annual information return that is used by the Canada Revenue Agency (CRA) to stop or mitigate underground economic activities within the construction industry in Canada.

Who Files a T5018 Slip?

The T5018 information return is to be filed by any corporation, partnership, trust or individual, that has construction as its source of primary business income. If your business generates more than 50% of its business income through construction activities, then you are required to file a T5018 information return.

Additionally, in a year, if you have made payments for construction services above $500 to subcontractors (or received credits from them), then you are also mandated to fill the T5018 slip.

Process for Filing an Information Return Slip

Residency status determines the specific information slip that’s to be completed.

Subcontractors who are residents of Canada are required to report contract payments on a Contract Payment Information Return. This information return consists of a T5018 slip and summary, and it covers construction services executed within and outside of Canada.

Subcontractors who are not Canadian residents are to complete the T4A-NR information return, which includes a T4A-NR summary and slip.

Regardless ofthe information slip you are to file, it can be done either by yourself or your accountant on the CRA website. It can be done via the My Business Account portal or Represent a Client portal respectively.You can file as many slips as needed via these portals on the CRA site.

When Are You to File the T5018 Return Information?

You can file the T5018 on a fiscal-year basis, or calendar-year basis. Regardless of the reporting cycle you choose, the return is due six months post the reporting period.

If you want to make changes to your current reporting period, you will need approval from the CRA.

Should your business stop operating, you are required to file the information return within 30 days post-closure of the business.

What Are the Penalties for Not Filing Your T5018 Return Information?

There are strict penalties for late submission or failure to submit your return information after the expiration of the reporting period.

Each slip is counted as separate information return, and the CRA will penalize you based on the number of slips submitted late - or not submitted at all. The number of late days is used to calculate the penalty fee.

Interest will continue to accrue on the penalty sum until it is paid in full.

Additionally, any contractor that cooperate with a subcontractor to conceal financials, to avoid taxes, could face criminal charges. They could also be penalized with fines up to 200% of the taxes they tried to evade.

Conclusion

The T5018 is the primary means the Canada Revenue Agency (CRA) uses to track financial activity between employers and subcontractors to ensure that all earnings and taxes are paid correctly and on time.

If you need help with filing T5018 forms, feel free to contact us at 778.801.5789 or email to jluk@bloomaccounting.ca

If you are a business in BC, you may have received a notice to register for the Employer Health Tax by May 15, 2019.

First off this only applies to businesses with $500K gross annual payroll or more in the last calendar year.

If you run multiple businesses, note that the $500K threshold is shared amongst associated businesses.

How to Register?

To Register: Visit the Etax BC log in page (same page you would log in to file PST) and you will find a link to register for Employer Health Tax.

How Much is the Tax?

For every $1 above $500K, expect to pay 2.925% up to payroll of $1.5mil.

For every $1 above $1.5M, expect to pay 1.95%

Much like corporate tax, installments are required to be made if EHT is more than $2925.

In other words, if you have more than $600K in gross annual payroll, you will need to make quarterly installments.

Knowify gives contractors construction software to handle job costing, contracts, estimates, job management, service tickets, time tracking, scheduling, invoicing, and billing. Knowify can help any commercial or residential contractor manage and grow their business. PLUS! It integrates with QuickBooks Online.

We recently put two cloud based contractor software to the test; Knowify vs. Co Construct.

How did both score?

What were the strengths and weaknesses?

Ready?

Lets Begin.....

Our Rating:

We scored Knowify at 8 / 10 and Co Construct 7 / 10 Based on the following factors

Proposals

Knowify definitely scored higher on the this feature. Proposals can be generated and sent out for E-signatures in Knowify vs. Proposals are generated in Co-Construct and exported to a word document. The ability to create, send and track proposals within one platform streamlines the contract process and ensures that all contracts are signed and found in one spot.

Invoicing

Knowify again scored higher with the ability to invoice within the software. Co construct does not have this feature at all.

We found it imperative for our clients to know total committed contract values, billed portion and unbilled portions in the pipeline in real time, and Knowify does the job. Both the invoices and payments are synced between Knowify and Quickbooks vs. Co Contract, no invoice, however payments are synced with Quickbooks.

Budgeting

Co-Construct won this feature over Knowify. We found it helpful to template job budgets and able to expand on each phase of a job and budget for both materials, multiple subcontractors, freight, and misc. supplies.

Change Orders

Both software creates change orders and sends out to client for electronic approval. Nice!

Again, Co-construct does not have an invoicing feature, so it would be imperative to ensure your Accounting team invoices the change order after its been approved. Where as Knowify will track the approved invoice as an unbilled portion of the change order.

However if your change order is an addition of an entire scope which requires additional budgeting, Co-Construct would be the software we recommend as Co-constructs's budgeting feature is more detailed and flexible compared to Knowify.

Job Costing

With Co-Construct, scopes can be templated and cost accounts assigned to each product / item.

With Knowify, same costing can be templated and is done through the Plan & Track module, however, lacks the ability to assign multiple sub contractors to each phase and for that reason Co-Construct wins slightly here.

Congrats! You are ready to onboard your first Employee!

Step 1: Obtain a CRA Payroll Number.

You can do this by simply giving CRA Business a call and a rep will issue a payroll number immediately.

The account number will be your business number followed by RP0001.

Step 2: Select Your Payroll Service Provider

There are ample payroll service providers available, such as Ceridian, Payworks, ADP to name a few.

Each of these providers offer an online platform to process your payroll, track vacation accruals, manage employee details, facilitate direct deposit, and issues ROE's upon termination.... for a fee. Fee structures varies between providers so read the fine lines! Late payroll or extra runs can cost up to $150. OUCH.

Another option is Quickbooks Online Payroll. If you are using a bookkeeper or DIY, you can add on the payroll module for ~$20 per month. QBO also facilitates direct deposit, however does not file your PD7A remittances for you. Your bookkeeper or yourself will need to do this monthly.

If you are wanting the FULL Service options which includes filing and remitting the monthly remittance to CRA, Quickbooks now offers Payroll Advance which costs ~$40 / month.

Regardless of which service provider you choose, its important to have someone knowledgeableto process your payroll as he / she will need to still calculate the statutory holiday pay if eligible, vacation pay, bonuses, commissions etc.

Step 3: Sign Employment Agreement & TD1 CRA forms

After extensive interviews and arriving at your employee of choice, it is customary to lay out the terms of the employment on paper and have both parties sign an employee agreement along with TD1 CRA Federal & Provincial forms.

Step 4: Process Payroll

Log in to the service provider chosen, process the payroll, cut check or process by direct deposit.

If you are using one of the full service providers, you will not need to issue pay stubs as your employee can log in to the self serve portal and access. If paying by check(s), pay stub(s) are printed and attached to the check(s).

Things to Remember

Payroll Remittances are generally paid monthly, by the 15th of the following month.

T4 are issued by Feb 28th of the following year. T4 Summary must be filed by Feb 28th of the following year.

Worksafe reports are filed either quarterly or annual depending on your business.

ROE's must be issued upon termination of an employee and filed with Service Canada.

Vacation & severance if any, must be paid out upon termination.

Not sure if employee qualifies for stat pay? See POST: http://bloomaccounting.ca/blog/view/274